The Water and Data Center Collision Is an Investment Thesis

The water problem with AI data centers is a question of location, not national supply. Why water efficiency is becoming a gating factor on the AI buildout, and an investable one.

Let’s start with a number that seems to settle the debate. Every data center on Earth, running for a full year, uses less water than U.S. agriculture uses in a single day. American farms consume roughly 118 billion gallons a day, and the entire global fleet of server farms does not approach that figure.

It’s easy to conclude that the AI water panic is overblown and that there’s nothing here worth a second look. That conclusion relies on a national average, which is the most misleading way to read this problem. For data centers, the water question is fundamentally about location. Once you account for where the water is actually being drawn, a culture-war headline turns into one of the cleaner infrastructure investment theses of the decade.

Why the national average misleads

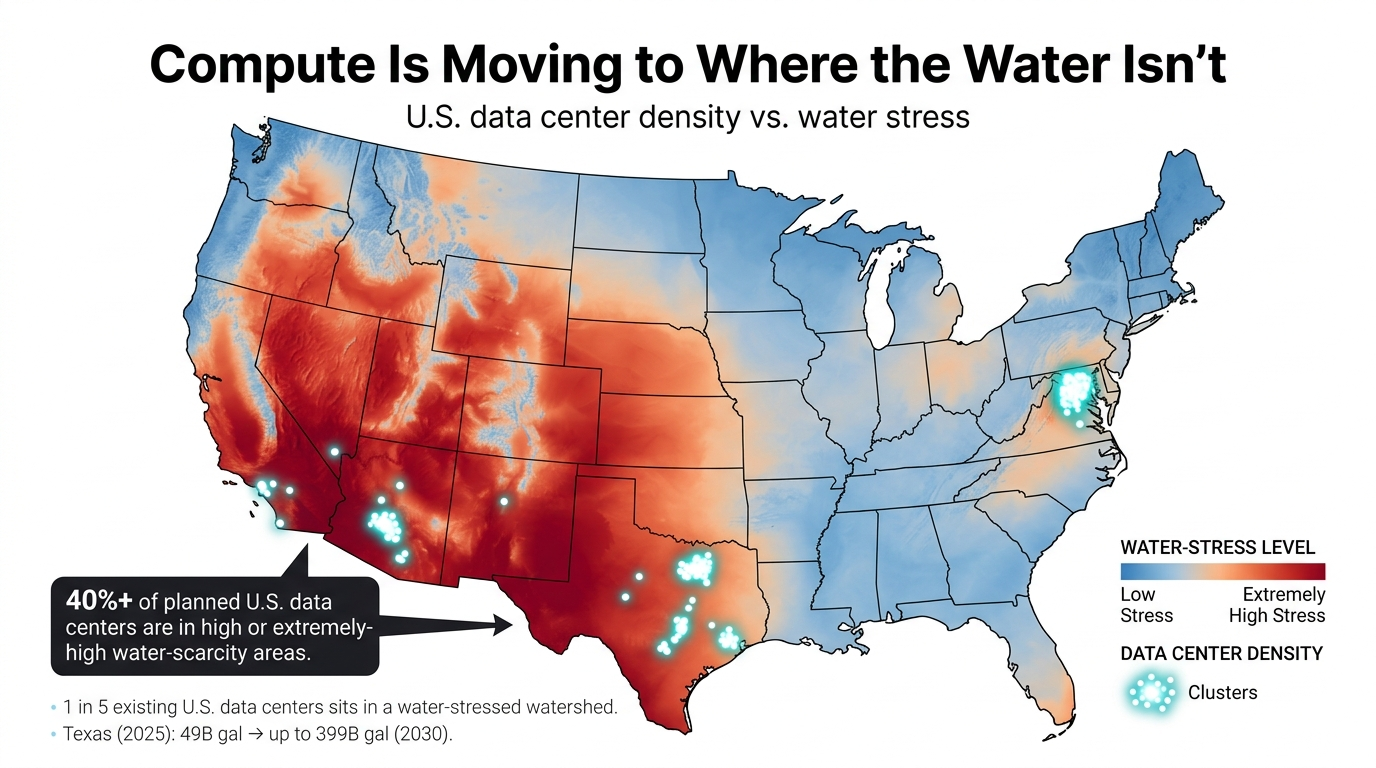

Roughly one in five U.S. data centers already sits in a watershed under stress, and more than 40% of planned facilities are slated for high or extremely high water-scarcity areas, according to analysis compiled by Bloomberg and the law firm Nixon Peabody. Compute is getting sited where land is cheap, power is available, fiber is dense, and tax incentives are generous, which in practice means Arizona, Texas, and Northern Virginia. Water almost never makes the site-selection shortlist.

That dynamic produces numbers like this. Data centers in Texas are projected to grow from about 49 billion gallons of water in 2025 to as much as 399 billion gallons a year by 2030, an eightfold jump, in a state where 85% of the land was in drought when that projection was published. The Lincoln Institute frames it as draining Lake Mead by more than 16 feet.

Nationally, water is cheap and abundant. In the exact places where the AI buildout is landing, it is scarce, contested, and increasingly political. That mismatch is the entire investment story.

Water became a gating factor

For investors, the shift from abundance to scarcity changes the calculation. For years, water was an ESG footnote in a data center pro forma, a sustainability bullet point for the CSR report. In 2026 it became a critical-path constraint. Where a developer cannot secure a water permit, the concrete does not get poured.

The evidence is accumulating. Tucson rejected “Project Blue” in August 2025 over water and energy concerns. Across the country, an estimated $64 billion in data center projects were delayed or canceled between mid-2024 and early 2025 in the face of organized local opposition, much of it water-driven. States are also codifying the friction. Minnesota’s HF 16 now requires water-appropriation permits for data centers using more than 100 million gallons a year, Virginia’s SB 1449 forces localities to study water and agricultural impacts before approving projects, and California is exploring an outright ban on using potable water for cooling.

This is what turns “water is scarce” from a vague worry into a concrete demand signal. Once water efficiency becomes a precondition for building at all, the companies that deliver it are selling something much closer to a building permit than a sustainability story.

Where the capital is flowing

The capital is already moving toward the companies that profit when gallons become the bottleneck. The headline action is in cooling. Evaporative cooling, the old approach, works by letting water evaporate to carry off heat, which is cheap on power and costly on water, with up to 85% of the water never returning. Closed-loop systems, including direct-to-chip and immersion cooling, recirculate fluid and use a small fraction of the water. Crusoe recently raised a $1.4 billion Series E (October 2025) on a closed-loop, direct-to-chip approach, and its 1.2-gigawatt Abilene site reportedly uses on the order of 12,000 gallons a year. Firmus Technologies pulled in $327 million for immersion-plus-direct-to-chip, and Corintis raised $24 million for in-chip microfluidic cooling and is running trials with Microsoft.

The broader category is growing quickly. The data center cooling market is forecast to exceed $20 billion by 2029, with liquid cooling growing roughly 39% a year. Blackstone backed a $925 million debt facility for Colovore, and Carrier put venture money into ZutaCore. An emerging niche, including companies like AirJoule, pulls usable water back out of waste heat, and on-site treatment and reuse are close behind.

There is an important caveat. Closed-loop cooling saves water but generally burns more energy, and if that power comes from a gas plant, the result is a trade of water for emissions, along with more water consumed upstream at the power plant. Water and energy are the same conversation, and you cannot optimize one in isolation. The companies that win will be the ones that land in the right place on the water-versus-energy curve for a given site, rather than the ones that simply use the least water. Sorting that out is where real diligence earns its keep.

What it means for investors

The reflexive take on data center water is a morality play, thirsty AI against parched communities. The investor’s version is more insightful. The binding constraint was never national water supply but permitting friction in specific, scarce, politically sensitive locations, and that constraint is hardening into law faster than the industry can engineer around it.

The durability of the thesis comes from the fact that this demand does not evaporate when a subsidy expires or sentiment shifts. As long as compute keeps chasing cheap land and power into water-stressed regions, every new facility becomes a forced buyer of water efficiency. The largest buyers already see it. Microsoft is rolling out zero-water cooling as a standard, Amazon is chasing a water-positive-by-2030 pledge, and Google has promised to replenish 120% of what it consumes. When buyers at that scale pre-commit, it signals a market forming rather than a passing trend.

The bottleneck on the AI buildout was first GPUs, then power. Increasingly the constraint is water, and specifically water in the wrong locations. For anyone writing checks in this space, the question worth asking is which companies hold a genuine permit-unlocking technology and which ones simply have a polished press release. At a distance the two look alike, and only one of them is worth backing.

At HydroKnowledge, we help investors and strategic partners evaluate moments exactly like this one, with diligence on water technology, market mapping, and go-to-market strategy in the water sector. If you are weighing a bet at the intersection of water and compute, let’s talk.

Related insights

Working on something in water?

HydroKnowledge works with water technology companies, utilities, and investors on go-to-market strategy, AI adoption, and advisory services.

Start a conversation