Where Smart Money Is Going in Water in 2026

Water-tech funding hit a record in 2024 yet remains a rounding error of cleantech capital. Where disciplined money is concentrating in 2026, and where it is not.

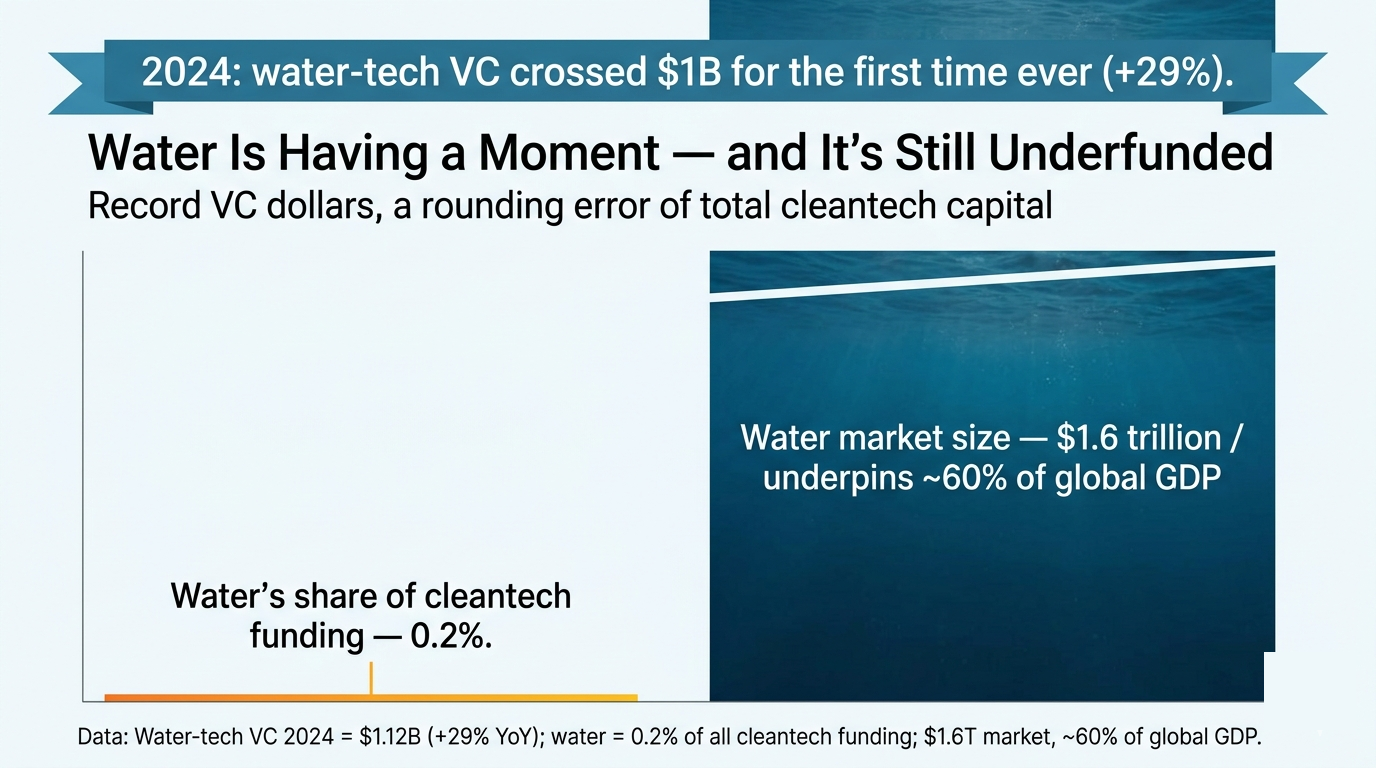

In 2024, water-tech venture funding crossed $1 billion for the first time in history, reaching $1.12 billion, up 29% in a single year. By that measure, water finally arrived and the smart money was pouring in.

The fuller picture is more sobering. That same year, water tech captured roughly 0.2% of all cleantech funding. Two-tenths of one percent, for an industry sitting on top of a $1.6 trillion market that underpins something like 60% of global GDP and, ultimately, all human life.

That gap defines water investing in 2026. The sector is having a genuine moment while remaining radically under-capitalized relative to its importance. The more useful question is not whether water is hot (the answer is that it kind of is, certainly in the communities I’m a part of), but where the smart money is concentrating.

I’ve spent 16 years in this sector and have personally raised or advised companies raising more than $500M across multiple water ventures. Here is where the committed capital is actually going, and why.

2026 is a big year

The water-tech investments made during the 2020 to 2022 vintage are now maturing, and the people who track this closely are forecasting an exit wave starting in 2026. In 2025 alone, the sector saw seven deals top $1 billion in liquidity events rather than raises.

The bigger shift is behavioral. Of the 383 investors who made a water bet in 2024, 303 were first-timers, and historically only about 250 of the nearly 1,500 investors who have touched water since 2018 ever came back for a second deal. Retention is brutal. Many investors show up, get burned by the long cycles, and leave.

The capital that remains has grown disciplined and selective. Investors now want proven technology, validated pilots, and a clear path to recurring revenue before they write a check. This is a flight to quality, and it determines which categories get funded.

Three accelerants doing the real work

A few macro forces are pushing water up the priority list, and they are what give the thesis legs beyond a single hype cycle.

PFAS regulation. The EPA’s limits on “forever chemicals” are creating an entire compliance market. In May 2026, the agency proposed keeping its PFOA and PFOS limits while giving water systems until 2031 to comply, which stretches the timeline without changing the inevitability. Every affected utility becomes a forced buyer of treatment.

Industrial and data-center water demand. Semiconductor reshoring, the AI buildout, and the broader energy transition are creating enormous new industrial water needs. Bluefield Research projects that the industrial water and wastewater market will exceed $62 billion a year by 2030. Texas data centers alone are projected to grow from 49 billion gallons of water in 2025 to as much as 399 billion by 2030.

Aging infrastructure. The unglamorous and unkillable driver. America’s pipes are old and someone has to pay for it.

There is a real counterweight to all of this, a federal funding cliff. The Infrastructure Investment and Jobs Act, which directed $50 billion to water over five years, expires September 30, 2026, and the reauthorization fight is live, with proposed EPA budget cuts hanging over the State Revolving Funds. Water-project awards in the first half of 2025 fell 53% year over year. Smart money is positioning for the demand while acknowledging that the policy tailwind is not guaranteed.

The three categories where capital is concentrating

The disciplined money is flowing into three areas.

Digital water and AI analytics. This is the most-funded sub-sector by deal count, for understandable reasons: software margins (at least for now… let’s see what happens with ‘vibe-coding’ hitting an all-time high), recurring revenue, and no 20-year concrete to pour. Bluefield projects that U.S. and Canada digital-water spend will double from $14 billion in 2026 to $29 billion by 2036. Leak detection, smart metering (already a $6.8 billion global market), predictive maintenance, and AI-driven optimization all fit the recurring-revenue model that investors understand well.

Industrial and ultrapure water, plus reuse. The unsexy giant. Semiconductor fabs and data centers need staggering volumes of ultrapure water, and closed-loop reuse can cut a fab’s freshwater withdrawals by up to 95%.

PFAS treatment. A regulation-driven market growing at roughly 6% a year, with North America holding about 42% of it. When the government mandates removal of a contaminant from every public water system in the country, the growth case writes itself, and the constraint becomes capacity.

The strategic deals show where the committed money sits. Ecolab bought Ovivo’s electronics ultrapure-water business for $1.8 billion (closed December 2025), a direct semiconductor and data-center play. EQT Infrastructure acquired Seven Seas Water Group, a 220-plant water-as-a-service operator, a private-equity bet on decentralized treatment. Veolia paid roughly $1.75 billion for the rest of its Water Technologies & Solutions arm. And Burnt Island Ventures closed its second fund at $50 million in October 2025, explicitly citing data-center demand. These are the players who know the terrain, buying more of it.

What it means for investors

Despite the record private funding and the billion-dollar M&A, the public proxies lagged in early 2026. The largest water ETF (PHO) was negative year-to-date. Xylem dropped more than 8% on cautious 2026 guidance and traded well off its highs. American Water sat about 16% below its 52-week peak.

That disconnect between frothy private markets and muted public ones tells you what kind of sector this is. Water rewards patience and domain knowledge rather than enthusiasm. The sales cycles are long, with two to three years or more between rounds being normal. The buyers are fragmented across thousands of utilities, the margins are regulated, and the field is full of strong technologies that never scaled because their backers didn’t understand how to sell into a century-old utility procurement process.

None of that is a reason to stay out, and it’s the reason the returns exist for the people who stay in. The edge here was never a hotter take on the macro trend, since everyone can read the same PFAS headline. The edge is knowing which of the three categories a given company actually lives in, whether its validated pilot would survive a real utility’s scrutiny, and how long the sales cycle truly runs before the recurring revenue arrives.

Everyone already knows water is important. The investors who do well in 2026 will be the ones who can distinguish a company that will survive the long, unglamorous slog to scale from one that is only visiting.

At HydroKnowledge, that is the judgment we help investors and strategic partners make, with diligence on water-tech opportunities, market mapping across the sub-sectors, and go-to-market strategy built for how the water industry actually buys. If you are sizing up a water bet in 2026, let’s talk.

Related insights

Working on something in water?

HydroKnowledge works with water technology companies, utilities, and investors on go-to-market strategy, AI adoption, and advisory services.

Start a conversation