How State Revolving Funds Work for Water Tech Vendors

State revolving funds move more water infrastructure money than every federal grant program combined. Most vendors selling to utilities still ignore them.

State Revolving Funds are the largest, most reliable source of water infrastructure money in the United States. They have existed for nearly four decades. In any given year they move more capital into utility projects than every shiny new EPA grant program combined. And most of the founders and salespeople selling into the water sector cannot name a single thing on their state’s current Intended Use Plan.

That gap is expensive. A vendor who learns about SRFs after a utility’s board has already approved a project is a year late. The funding source was chosen during scoping. The eligible scope was defined when the project was nominated. The procurement that finally appears is the documentation of a decision that closed months earlier, and the line item that would have held your product is now sized for somebody else’s.

What an SRF actually is

There are two of them. The Clean Water State Revolving Fund (CWSRF) was created in 1987. The Drinking Water State Revolving Fund (DWSRF) followed in 1996. Together they have moved more than $200 billion into water and wastewater infrastructure over their lifetimes. They are administered by states, not by the EPA directly, which is the first thing most outsiders get wrong.

The mechanism is simple (in theory). Each year the federal government issues a capitalization grant to every state from EPA appropriations. The state matches a portion of that grant from its own funds. The combined pool is then used to issue loans, mostly at below-market rates, to local utilities for eligible infrastructure projects. As the utilities repay those loans, the principal and interest flow back into the state’s fund and are loaned out again. That is the revolving part. In many states the original federal seed money has turned over multiple times.

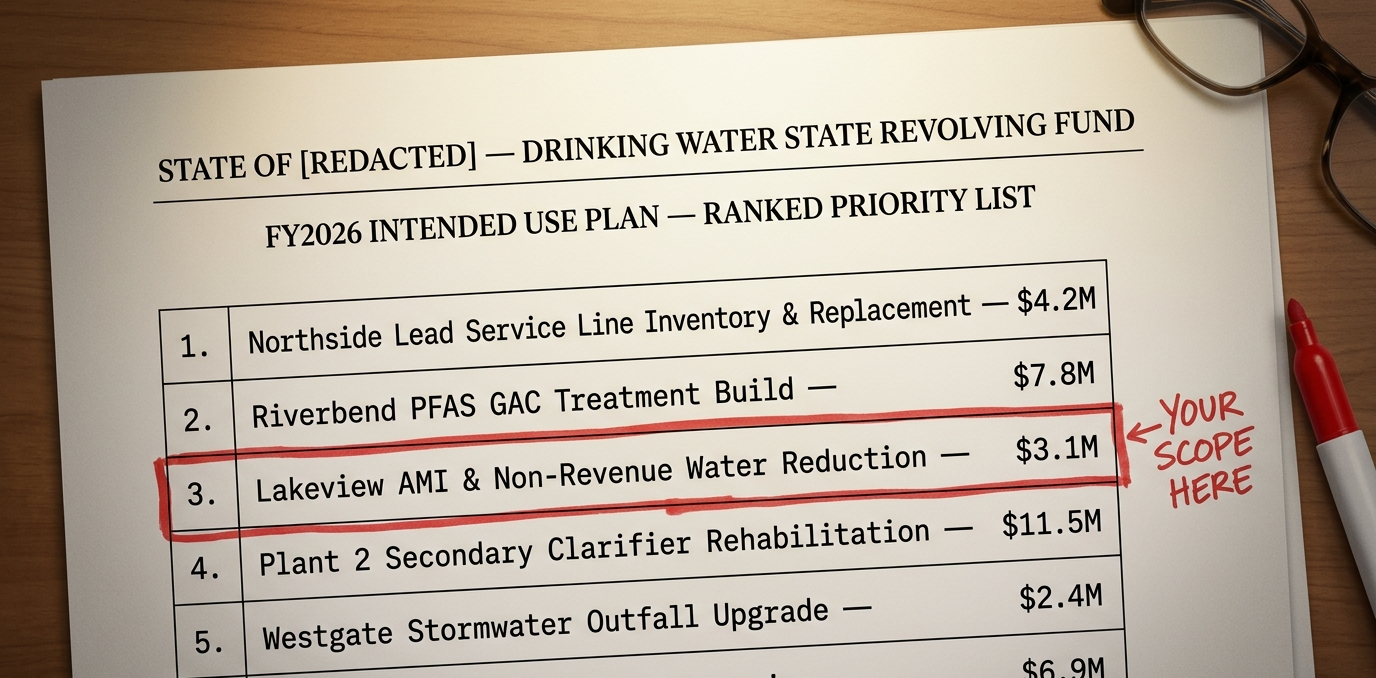

The catch, and the part most vendors miss, is what counts as an ‘eligible project’. Eligibility is determined by the state, against EPA guidelines, and is published every year in a document called the Intended Use Plan. The IUP is where the state writes down its priorities for the coming cycle, ranks the projects it intends to fund, and explains the formulas it uses for ranking. It’s basically the sales pipeline for everyone who sells anything that goes into a water or wastewater project. If your category is not represented on the IUP, or if you do not understand where it could fit, you are pitching against an invisible scoreboard.

How the cycle works

Every state runs its own annual nomination cycle, usually with applications due in the late summer or early fall. Utilities submit their proposed projects with a preliminary engineering report, an environmental review pathway, a cost estimate, and a financial picture. The state ranks the submissions against public-health risk, compliance need, affordability, and a handful of state-specific criteria. The ranked list becomes the IUP. The top of the list gets funded. Everything else either waits for the next cycle or gets bumped up by a withdrawal somewhere above it.

This timing has real consequences for vendors. A utility that decides in February that it wants to do something usually cannot pull SRF money in for that fiscal year. The slot in the IUP closed months earlier. The practical move is to be present in the project shaping conversations the spring or summer before the application window, when the utility is deciding which projects to nominate and how to scope them. By the time procurement opens the funding source is already chosen and the eligible scope is already defined. Vendors who do not understand how those scoping decisions get made are usually surprised to learn that a six-figure technology choice was settled in a forty-minute internal meeting they were never invited to.

What changed under the Bipartisan Infrastructure Law

The IIJA, signed in 2021, dropped roughly $43 billion of new capitalization into the SRFs over five years on top of the normal annual appropriations. That alone would be a meaningful boost. The more consequential change was how Congress structured a large share of that money. A significant portion of the IIJA SRF dollars must be issued as forgivable principal, which in practice means it functions as a grant. Some states are pushing forgivable percentages above 80 for projects in disadvantaged communities, lead service line replacement, and emerging contaminants like PFAS.

The result is that the same SRF program that has existed since the late 1980s is, for a few specific use cases, currently the most generous funding source in the federal toolbox. A vendor whose product fits inside an LSL inventory, a PFAS treatment build, or a disadvantaged-community drinking water project is selling into a funding stack that may be 80 to 100 percent forgiven. That changes the conversation about affordability in ways most pitch decks have not caught up to. The broader IIJA funding landscape covers how these set-asides connect to the other federal vehicles.

The strings

SRF money carries federal cross-cutter requirements that surprise vendors who have only sold to utilities funded by local rates and bonds. Three of them matter most for technology suppliers.

American Iron and Steel (AIS). Any iron and steel products permanently incorporated into an SRF-funded project must be produced in the United States. This applies to pipe, fittings, valves, hydrants, meter bodies, and a long list of other components. AIS waivers exist but are slow and uncertain. If your product contains meaningful iron or steel content and is not AIS-compliant, you are not selling into SRF projects without a serious conversation about manufacturing.

Davis-Bacon prevailing wages. Construction labor on SRF-funded projects must be paid at the federally determined prevailing wage. This raises installation cost and changes which contractors will bid. It does not affect product price directly, but it shapes how utilities scope projects and which integrators they trust.

Federal environmental review and procurement rules. SRF projects pull in a layer of NEPA-equivalent state review, competitive procurement requirements, and Build America Buy America (BABA) compliance. Sole-source procurements that work fine in a rate-funded project often will not survive an SRF audit. Vendors whose preferred sales motion is a no-bid pilot need to plan a path to an open procurement before the funding hits.

None of this is impossible. All of it is information you want before, not after, your champion at the utility starts drafting an IUP submission.

Three moves for vendors

The point of understanding SRFs is to use them. Three practical moves matter more than the rest.

First, read your state’s current IUP. Every state publishes it, usually on the environmental or health agency website. The document is typically 30 to 80 pages and contains the ranked project list, the funding formulas, and the set-aside priorities for the year. It tells you which utilities have funded projects in motion, what those projects look like, and where the state is steering money. Reading three IUPs from your top target states is, hour for hour, one of the highest-leverage research tasks a water founder can do.

Second, learn your state’s nomination calendar and work backward from it. If applications are due September 1, your champion at the utility needs scope, cost, and engineering support locked by July. Which means your conversation about scope needs to happen in May or June. Showing up in October with a great product and asking when budget opens is a year of lost time.

Third, decide early whether you are AIS-compliant, whether you can become AIS-compliant, or whether you need a sales motion that routes around SRF funding entirely. There is no shame in any of those answers. The mistake is leaving the question unanswered until a procurement officer raises it at the worst possible moment.

The utilities that move infrastructure dollars are, for the most part, moving SRF dollars. Vendors who understand that are pitching into a known pipeline. Vendors who do not are wondering why the funding never seems to be there.

HydroKnowledge helps water technology companies build go-to-market strategies that account for how utilities actually fund their work. Get in touch if you want a second pair of eyes on your funding strategy.

Related insights

Working on something in water?

HydroKnowledge works with water technology companies, utilities, and investors on go-to-market strategy, AI adoption, and advisory services.

Start a conversation